All Categories

Featured

Table of Contents

Area 691(c)( 1) supplies that an individual who consists of a quantity of IRD in gross income under 691(a) is allowed as a reduction, for the very same taxable year, a section of the estate tax obligation paid because the incorporation of that IRD in the decedent's gross estate. Usually, the quantity of the reduction is computed utilizing inheritance tax worths, and is the quantity that births the same proportion to the estate tax obligation attributable to the internet value of all IRD products consisted of in the decedent's gross estate as the value of the IRD consisted of in that individual's gross income for that taxable year births to the value of all IRD things consisted of in the decedent's gross estate.

Rev. Rul., 1979-2 C.B. 292, addresses a situation in which the owner-annuitant acquisitions a deferred variable annuity contract that offers that if the owner passes away prior to the annuity beginning date, the called beneficiary might choose to receive the existing accumulated worth of the contract either in the form of an annuity or a lump-sum repayment.

Rul. 79-335 concludes that, for functions of 1014, the agreement is an annuity explained in 72 (as after that effectively), and consequently obtains no basis modification by reason of the owner's fatality since it is regulated by the annuity exception of 1014(b)( 9 )(A). If the recipient chooses a lump-sum settlement, the unwanted of the quantity received over the quantity of consideration paid by the decedent is includable in the beneficiary's gross earnings.

Rul. Had the owner-annuitant surrendered the contract and got the amounts in unwanted of the owner-annuitant's financial investment in the contract, those quantities would certainly have been earnings to the owner-annuitant under 72(e).

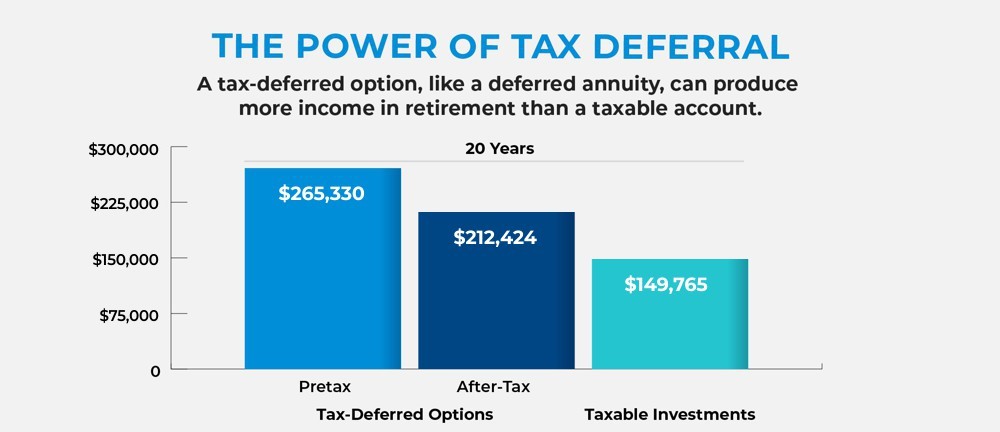

Immediate Annuities death benefit tax

In the present case, had A gave up the agreement and received the quantities at problem, those amounts would certainly have been income to A under 72(e) to the level they surpassed A's financial investment in the agreement. Appropriately, amounts that B gets that go beyond A's investment in the agreement are IRD under 691(a).

Rul. 79-335, those amounts are includible in B's gross earnings and B does not receive a basis adjustment in the contract. Nevertheless, B will certainly be entitled to a reduction under 691(c) if estate tax was due by reason of A's fatality. The outcome would certainly be the same whether B gets the survivor benefit in a round figure or as routine repayments.

The holding of Rev. Rul. 70-143 (which was withdrawed by Rev. Rul. 79-335) will certainly continue to get deferred annuity agreements bought prior to October 21, 1979, including any kind of contributions put on those contracts pursuant to a binding commitment participated in prior to that day - Structured annuities. DRAFTING details The primary writer of this income judgment is Bradford R

Q. Just how are annuities strained as an inheritance? Is there a distinction if I acquire it directly or if it mosts likely to a trust for which I'm the recipient?-- Preparation aheadA. This is a fantastic concern, but it's the kind you should take to an estate preparation attorney who recognizes the information of your scenario.

What is the connection in between the dead proprietor of the annuity and you, the beneficiary? What sort of annuity is this? Are you inquiring about income, estate or estate tax? We have your curveball question about whether the result is any various if the inheritance is with a trust fund or outright.

Let's begin with the New Jacket and federal estate tax effects of inheriting an annuity. We'll presume the annuity is a non-qualified annuity, which indicates it's not component of an IRA or various other competent retirement plan. Botwinick stated this annuity would be included to the taxable estate for New Jacket and government inheritance tax purposes at its day of fatality worth.

Do beneficiaries pay taxes on inherited Structured Annuities

citizen partner surpasses $2 million. This is called the exemption.Any amount passing to an U.S. resident spouse will certainly be completely excluded from New Jacket estate taxes, and if the proprietor of the annuity lives throughout of 2017, then there will certainly be no New Jacket inheritance tax on any type of amount since the estate tax is scheduled for abolition beginning on Jan. Then there are government estate taxes.

The present exception is $5.49 million, and Botwinick said this tax is probably not vanishing in 2018 unless there is some significant tax reform in an actual hurry. Fresh Jersey, federal estate tax regulation supplies a full exemption to amounts passing to surviving united state Following, New Jersey's inheritance tax.Though the New Jacket inheritance tax is arranged

to be repealed in 2018, there is noabolition set up for the New Jersey estate tax, Botwinick said. There is no federal inheritance tax obligation. The state tax obligation gets on transfers to everyone apart from a particular class of people, he said. These include spouses, youngsters, grandchildren, parent and step-children." The New Jacket inheritance tax puts on annuities simply as it uses to other assets,"he stated."Though life insurance payable to a specific beneficiary is excluded from New Jacket's estate tax, the exemption does not relate to annuities. "Now, revenue taxes.Again, we're assuming this annuity is a non-qualified annuity." In short, the earnings are tired as they are paid. A portion of the payment will be dealt with as a nontaxable return of investment, and the incomes will be exhausted as average revenue."Unlike acquiring various other assets, Botwinick claimed, there is no stepped-up basis for inherited annuities. If estate taxes are paid as an outcome of the addition of the annuity in the taxable estate, the beneficiary might be qualified to a deduction for acquired income in regard of a decedent, he claimed. Annuity settlements contain a return of principalthe money the annuitant pays into the contractand interestearned inside the agreement. The passion section is strained as regular income, while the major amount is not tired. For annuities paying over a much more prolonged period or life expectancy, the major section is smaller sized, leading to fewer taxes on the regular monthly settlements. For a wedded pair, the annuity contract might be structured as joint and survivor to ensure that, if one spouse dies , the survivor will continue to obtain surefire payments and appreciate the same tax obligation deferment. If a beneficiary is called, such as the couple's children, they end up being the recipient of an acquired annuity. Beneficiaries have multiple options to take into consideration when selecting just how to receive money from an acquired annuity.

{kind=link}

Table of Contents

Latest Posts

Exploring the Basics of Retirement Options A Comprehensive Guide to Variable Annuity Vs Fixed Annuity What Is the Best Retirement Option? Pros and Cons of Various Financial Options Why Choosing the Ri

Highlighting Variable Annuity Vs Fixed Indexed Annuity Key Insights on Choosing Between Fixed Annuity And Variable Annuity What Is the Best Retirement Option? Features of Indexed Annuity Vs Fixed Annu

Exploring the Basics of Retirement Options Everything You Need to Know About Financial Strategies What Is Tax Benefits Of Fixed Vs Variable Annuities? Features of What Is Variable Annuity Vs Fixed Ann

More

Latest Posts